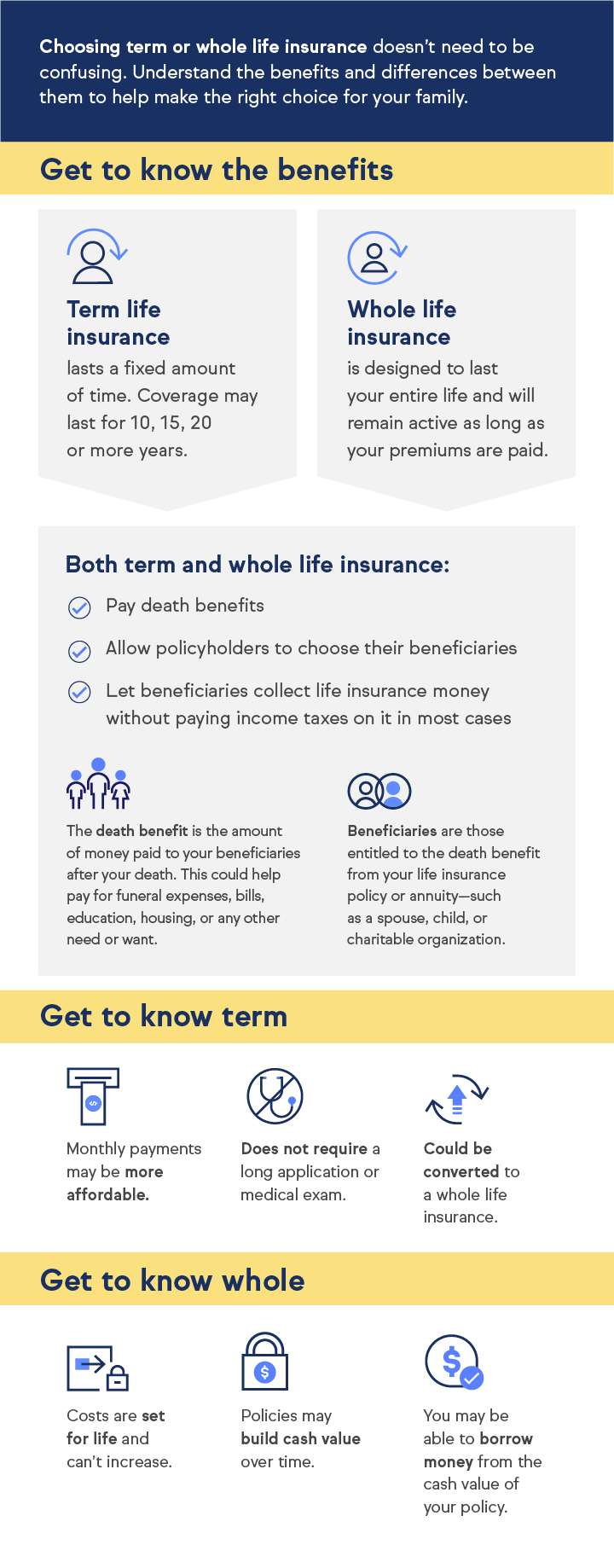

Understanding the Benefits of Whole Life Insurance: A Comprehensive Guide

Whole life insurance is a type of permanent life insurance that provides both a death benefit and a cash value component. One of the main benefits of whole life insurance is its ability to provide financial security throughout your entire life. As long as the premiums are paid, the policy remains in force, ensuring that beneficiaries receive a guaranteed payout upon the policyholder's death. This makes it an excellent choice for individuals looking to support their family's financial future, cover final expenses, or even make an inheritance.

In addition to the death benefit, whole life insurance policies accumulate a cash value over time, which can be accessed through policy loans or withdrawals. This cash value grows at a steady rate, providing policyholders with a reliable savings component that can be utilized for various financial needs, such as funding a child's education or managing unexpected expenses. Moreover, the cash value grows on a tax-deferred basis, allowing for more significant growth potential. Understanding these benefits of whole life insurance is crucial for making informed decisions about your financial planning and future security.

Is Whole Life Insurance Right for You? Key Factors to Consider

Whole life insurance is a long-term financial product that provides not just a death benefit, but also a cash value component that grows over time. Before deciding if it is right for you, consider your financial goals, your age, and your family situation. For instance, if you're looking for lifelong coverage that can potentially serve as an investment vehicle, whole life insurance might be a suitable choice. Conversely, if your primary goal is to secure temporary coverage, then term life insurance could be more appropriate. Additionally, assess your ability to commit to the typically higher premiums associated with whole life policies.

Another critical factor to weigh is your understanding of how whole life insurance works. This includes knowing the implications of borrowing against the cash value and the effects on your death benefit. It's advisable to consult with a qualified financial advisor who can provide personalized insights tailored to your financial circumstances. Remember, the decision should align with your overall financial strategy and life stage. By taking the time to evaluate these key considerations, you can make a more informed choice about whether whole life insurance is indeed the right fit for you.

The Timeless Appeal of Whole Life Insurance: Why It Matters Today

In a world where financial products come and go, whole life insurance stands out for its lasting value. Unlike term life insurance, which provides coverage for a limited time, whole life insurance combines a death benefit with a cash value component that grows over time. This dual benefit ensures that policyholders are not only protected in the event of an untimely death but also accumulate a financial resource that can be borrowed against or withdrawn if needed. As people increasingly seek stability and peace of mind in their financial planning, the appeal of whole life insurance remains as strong as ever.

Furthermore, the importance of whole life insurance becomes even more pronounced in today's economic climate, where uncertainties loom large. With its guaranteed cash value growth and fixed premiums, whole life insurance offers a dependable solution for those looking to secure their family's financial future. Many consumers are turning to whole life policies as a hedge against inflation, enhancing their financial strategy in an unpredictable market. Ultimately, the timeless appeal of this insurance product lies in its unique ability to provide both security and investment potential, making it a relevant choice for today's savvy consumers.